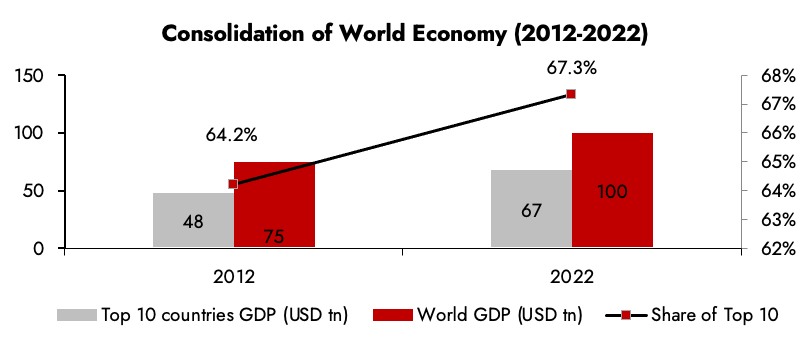

Consolidation of World Economy –

The financial world around us has been consolidating. Stronger entities have and continue to become stronger due to capitalizing on inherent strengths and the efficient use of capital. There’s no better evidence of the same than the world’s GDP and the increasing contribution of the larger economies to the world’s GDP. (Exhibit 1) This exhibit also reinforces our belief of K-Shaped recovery, on which we wrote a note in September 2020.

The GDP for the top 10 countries has increased at a much faster 3.4% CAGR v/s 2% CAGR for all other countries over the past decade.

Exhibit 1: Growth in the world economy has been driven by larger economies

Source: Ambit Asset Management, IMF

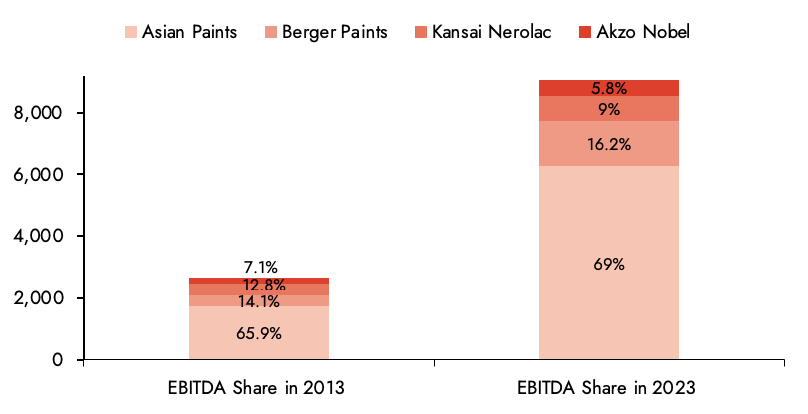

Consolidation of profit pools -

When larger economies are consolidating and garnering incremental market share, it’s no surprise to see the phenomena being replicated in well-run larger Indian companies. Well-run Indian companies such as Asian Paints have been able to consolidate profit pools in their respective markets while trying to expand their market into adjacencies. (Refer Exhibit 2)

Exhibit 2: Asian Paints profit market share has continued to increase over the past decade

Source: Ambit Asset Management, Company, Screener. Y axis refers to the EBITDA in crores.

Similarly, we have seen similar trends in retail where Reliance Retail and Avenue Supermarts have consolidated the majority of the profit pool of the industry.

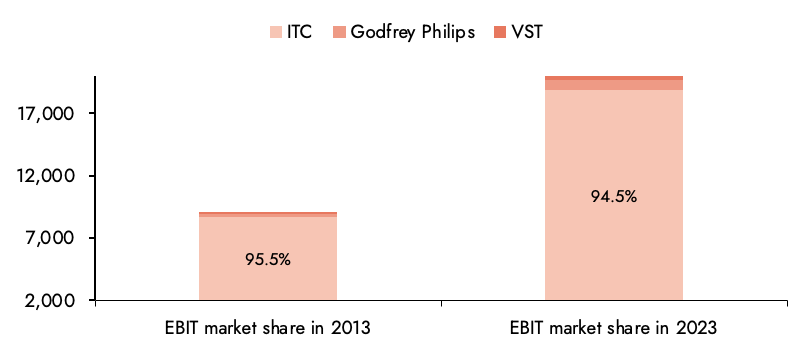

Consolidation to cannibalization –

The era of consolidation saw large companies becoming larger participants in the profit pool. But the larger you become, growing incrementally disproportionately to the industry size starts becoming more and more difficult. The relative size of the larger players makes it extremely difficult to continue growing at rates materially above the industry growth rate when you have a sizable market share (Refer Exhibit 3).

Exhibit 3: ITC’s profit pool in cigarettes is virtually the entire profit pool of the industry

Source: Ambit Asset Management, Company, Screener. Y axis refers to the EBIT in crores. For ITC and Godfrey Philips – Only segments related to cigarettes and tobacco products have been considered.

With substantial cash flows and very healthy financial matrices, we’ve seen multiple entities across sectors venturing or significantly strengthening their presence in non-core areas with the intention of increasing their addressable market size resulting in longevity of growth.

Corporate Cannibalization (Cannibalization) refers to one company impacting another company’s profits.

Take the example of ITC, garnering almost ~95% of the cigarette industry profit pool, healthy ROCE and solid cash flows from the cigarettes business has resulted in the company entering into other segments in search for growth which in turn has cannibalized profit pools of other sectors - FMCG, Packaging, Agriculture, IT and Hotels.

Similarly, we have seen large conglomerates diversifying into non-core areas having seen their profit pools and growth rates moderate.

The competitive intensity has increased multi-fold in non-core areas in the recent past.

|

Conglomerates |

Core Areas |

Diversified Areas (Current or past) |

|

Reliance Industries |

Oil, Gas and Petrochemicals |

Telecom and Internet, Retail, Green Hydrogen, Consumer Lending, FMCG. |

|

Adani Enterprises |

Commodities, Infrastructure, Power |

Data Centres, Green Energy |

|

Tube Investments (Murugappa Group) |

Engineering, Metal Products |

Electrical Equipment, Electric Mobility, API / CDMO Manufacturing |

|

Aditya Birla Group |

Cement, Commodities, Financial Services, Fashion and Retail |

Paints, Gold Retail. |

|

Tata Group |

IT, Steel, Auto, Lending, Power, Consumer Goods, Chemicals |

E-commerce, EV-battery and charging infrastructure. |

Apart from the above examples, competitive intensity has been rampant across almost sectors and sub-segments.

We bring to attention the rising competitive intensity in sectors such as Building Material (Pipes, Sanitary and Faucet ware, Wood Panel, Paints, Adhesives etc.) and FMEG (Room Air Conditioners, Electric Appliances, Fans etc.) from both incumbents (Astral, Havells etc.) along with newer entrants such as Atomberg and Polycab.

While consolidation of the profit pool as a story continues at a slower rate. The era of cannibalization has begun, and while it’s early days it is important to assess –

- Which companies are likely to be successful in cannibalizing profit pools?

- Which companies are likely to defend their profit pools from being cannibalized?

- Which sectors run a risk of profit pools being suppressed due to intense competition?

Which companies are likely to be successful in cannibalizing profit pools?

We take forward the example of Asian Paints in Exhibit 2.

For Asian Paints, to grow larger in size over the past decade the company has aggressively forayed into non-core categories for Paints such as -

- Putties – a stronghold primarily by Cement majors

- Waterproofing and Adhesives – Pidilite being the market leader at the time of entry

- Home Improvement - Bathware / Kitchenware / Lighting etc.

Of the above, Asian Paints has been successful in cannibalizing profit pools of other segments to varying degrees of success.

Putties and Water-proofing continue to be solid growth drivers both on the top and bottom line.

Home Improvement on the other hand has been a laggard with the company yet to have any share in the profit pool despite its presence over the last 7-8 years.

The above measures along with continued market share gains on the traditional paints business has resulted in Revenue / EBITDA CAGR for Asian Paints for the last decade to be 13% / 14%, which is substantially higher than the industry growth rate.

However, the growth has come at a cost of deterioration in return ratios. ROCE for Asian Paints has dropped from ~47% in FY 2013 to ~32% in FY 2023, a large part attributed towards diversification into the above categories which are inherently lower ROCE businesses.

Thus, when entering a newer category we see the growth comes at the cost of return matrices. Thus, the likelihood of success in cannibalizing of profit pools increases materially when the return matrices (ROCE’s / Cash Flows) are higher.

Which companies are likely to defend their profit pools from being cannibalized?

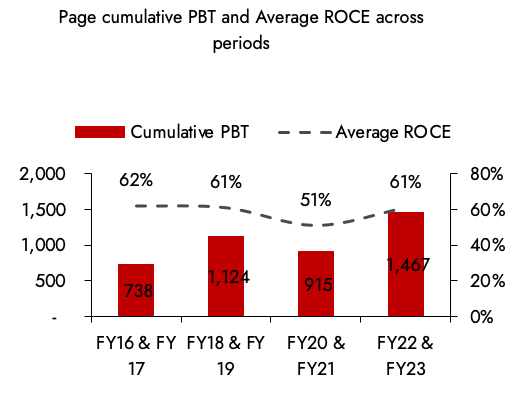

The inherent strength of a company in the longer run is demonstrated by its ability to withstand competition and defend profit pools. Take the case of Page Industries, the market leader in the innerwear segment.

In FY 2016, the company reported a PBT of 343 crores with a staggering ROCE of 62%, while doubling its PBT in the past 3 years. (>25% CAGR).

Such solid growth rates and operational matrices reported by Page Industries, resulted in competition attempting to cannibalize the profit pool, particularly Aditya Birla Fashion and Retail (ABFRL) via Van Heusen innerwear and athleisure in 2016.

In FY2016, ABFRL despite having a presence across man and woman’s formal and ethnic wear segments along with retail presence in Pantaloons did a LBT of -110 crores with an ROCE of 5%.

Van Heusen aggressively attempted to scale up its offering primarily in 2018-19 trying to cannibalize profit pools by increasing competitive intensity owing to tactics such as price undercutting, higher incentives to channel partners and an increase in marketing spends resulted in a slowdown in growth and squeezing of profit pools for the entire industry.

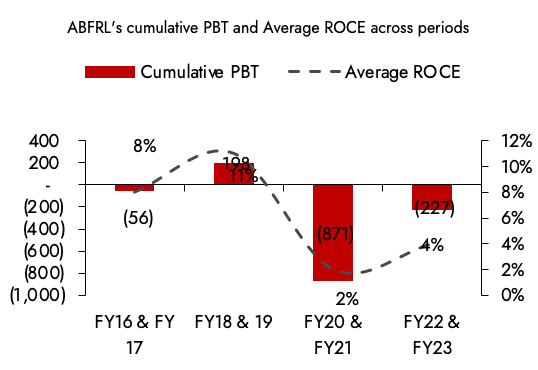

Exhibit 4: Page Industries has been able to defend and further consolidate its profit pool while maintaining their return ratios

Source: Ambit Asset Management, Screener

Exhibit 5: ABFRL however on the other hand have been unable to garner a sizable profit pool or improve their return matrices

Source: Ambit Asset Management, Screener

However, once the initial investments peaked out without any material gains, the competitive intensity subsided and Van Heusen failed to cannibalize the profit pool and Page Industries continued to substantially outgrow and garner a higher market share due to the inherent strengths of the business (i.e. distribution and branding). (Refer Exhibits 4 and 5)

The impact on incumbent leaders is dependent on how strong the leader in the market is along with the quantum and efficiency of capital deployed by the companies trying to cannibalize profits.

Thus, we come to a similar conclusion that a company demonstrating great return matrices and a historical track record of efficient capital allocation is more likely to be insulated against the cannibalization of its profits.

Which sectors run a risk of profit pools being suppressed due to intense competition?

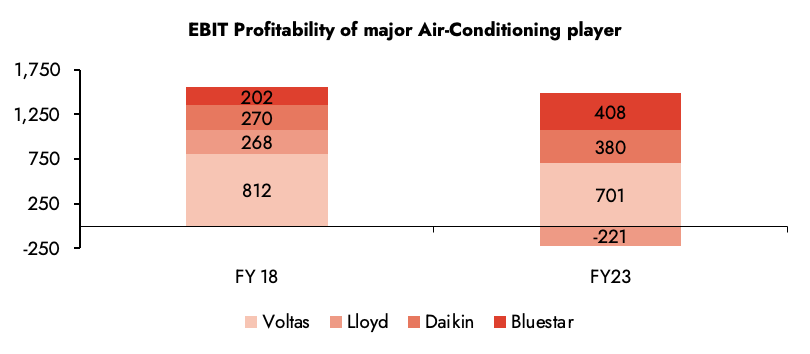

The AC market has no distinct market leader and its profit pool has been shared by multiple players. While Voltas remains a market leader in the Room Air Conditioners (RAC) segment, it’s not a runaway leader by any means.

An increase in competitive intensity especially from Havells (via Lloyds) and Daikin(the world’s largest air conditioner company) along with increased aggression from existing peers such as Blue Star has resulted in a profitability squeeze for market leaders such as Voltas over the past few years.

Exhibit 6: Profit Pool of Air Conditioning majors has seen a big squeeze over the last 4 years

Source: Ambit Asset Management, Company

As seen above, the total industry profitability of the top 4 players dropped dramatically from 1553 crores to 1268 crores owing to sustained competitive intensity, this is despite revenues for the industry almost doubling from 15500 crores to 29608 crores.

With no signs of reducing intensity, the sector ROCE / profitability matrices may remain under pressure in the foreseeable future.

A sector’s profit pool is likely to be squeezed due to either the presence/entry / increased aggression of multiple deep-pocketed players with formidable return matrices in an industry with no clear distinctive leader.

Conclusion

We come to the conclusion that the winners of the cannibalizing profit pools will be companies with a track record of efficient capital allocators, strong balance-sheet, reasonable risk appetite and access to capital.

In a dynamic economy, we anticipate some of our portfolio companies to be either cannibalizing profit pools or/and defending their profit pools.

Our focus is on evaluating incremental capital allocation along with the right to win in a proper category on a case-to-case basis. A successful cannibalizing strategy may result in profit pool opportunity being huge enough to take care of incremental growth over the long term.

We also closely relook at inherent strengths and the ability of management to defend their core profit pools.

We anticipate a majority of our portfolio companies to be the key beneficiaries of both consolidation and cannibalization themes .

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has an unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced with disruptions at regular intervals. As the industry evolves or is faced with disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

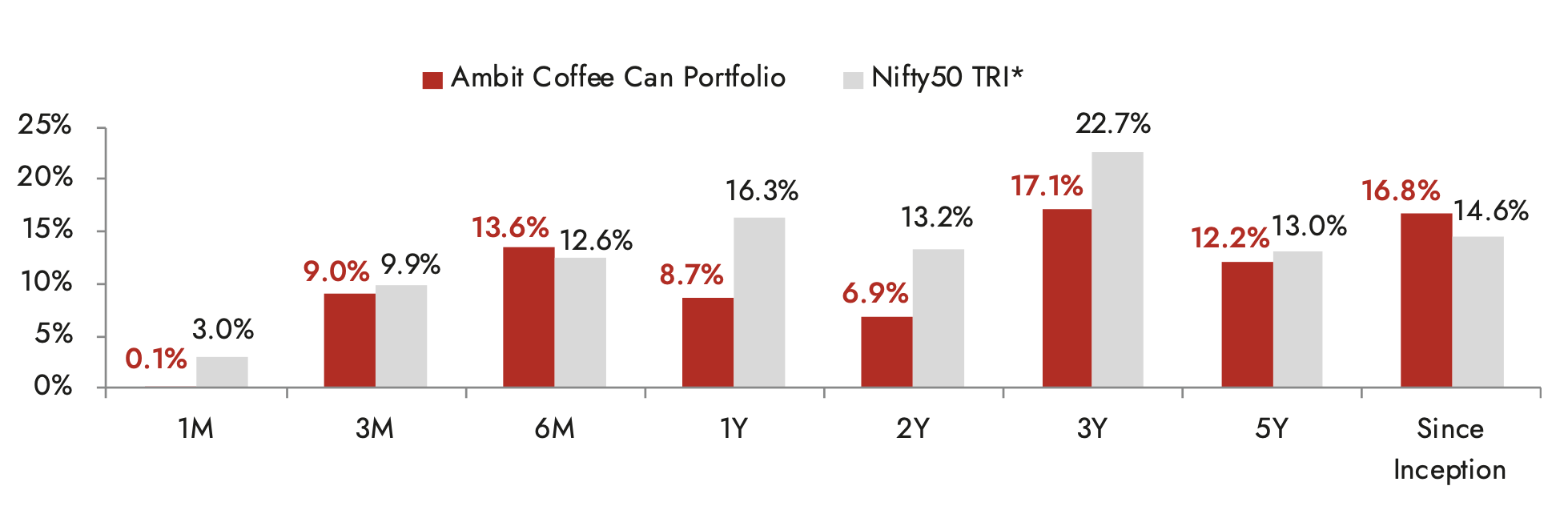

Exhibit 7: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of May 31st 2023; All returns are post fees and expenses; Returns above 1 year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.* Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI. In addition to the same, we have included the MF peer average for information purpose only. The same should not be relied upon for performance benchmarking in any manner. MF Peers include: Aditya Birla Sun Life MF, Franklin India MF, HDFC MF, ICICI Prudential MF, Nippon India MF, SBI MF.

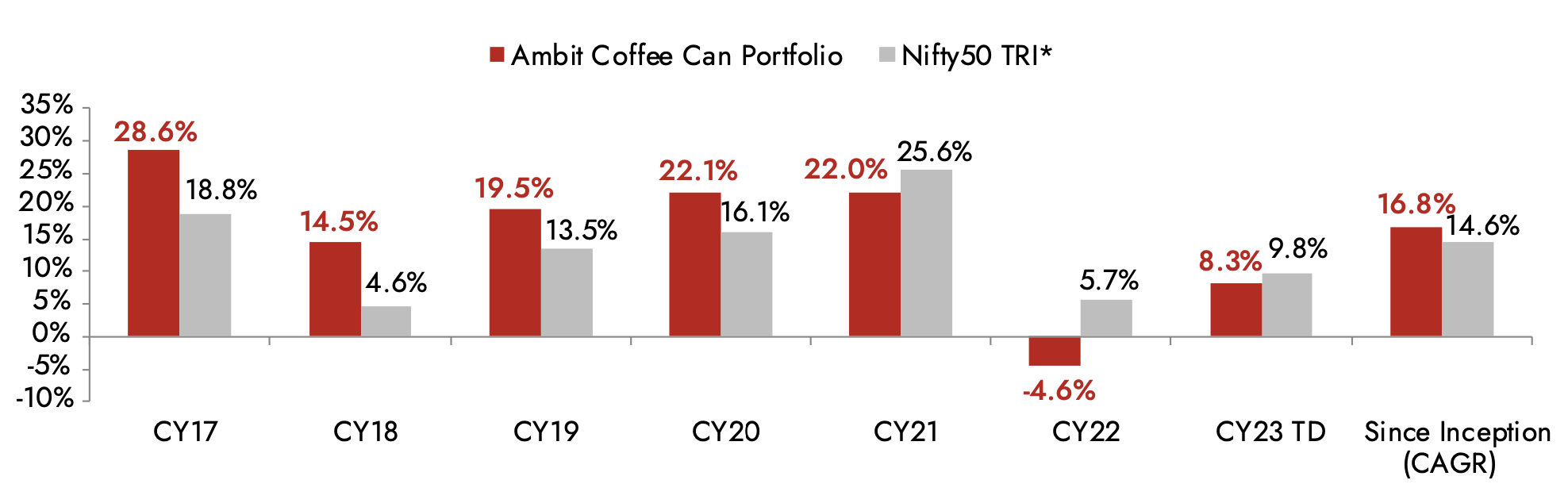

Exhibit 8: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of May 31st 2023; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

* Nifty 50 TRI is the selected benchmark for the Ambit Coffee Can Portfolio and the same is reported to SEBI. In addition to the same, we have included the MF peer average for information purpose only. The same should not be relied upon for performance benchmarking in any manner.

MF Peers include: Aditya Birla Sun Life MF, Franklin India MF, HDFC MF, ICICI Prudential MF, Nippon India MF, SBI MF.

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with these compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

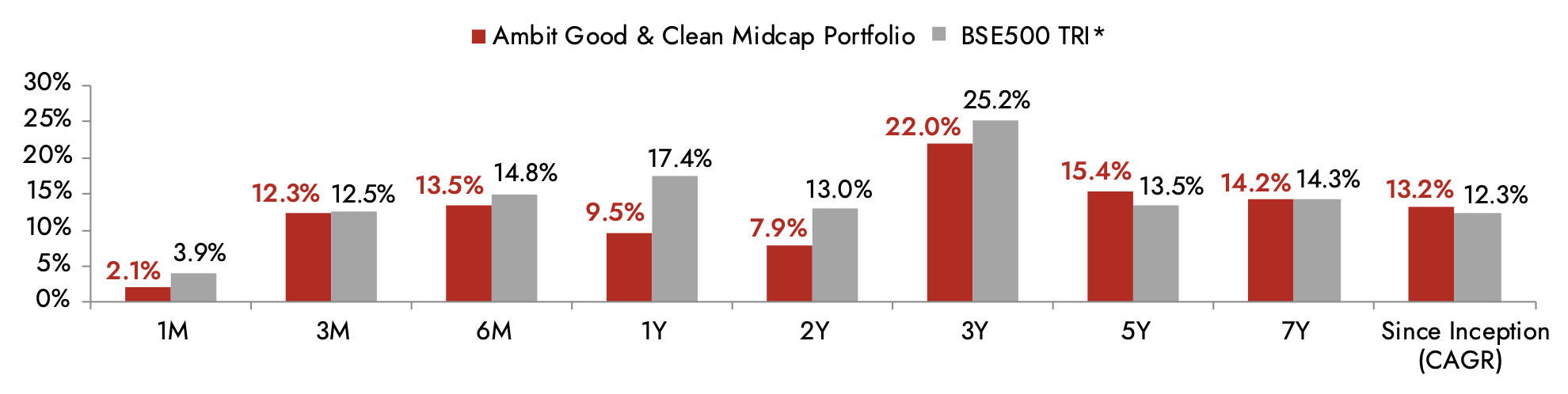

Exhibit 9: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of May 31st 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses.

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI. In addition to the same, we have included the Nifty Midcap 100 and MF Peers for information purposes only. The same should not be relied upon for performance benchmarking in any manner. MF Peers: HDFC MF, Kotak MF, SBI MF, Franklin India MF, Aditya Birla Sunlife MF, Axis MF, L&T MF, MOSL MF, ICICI Prudential MF

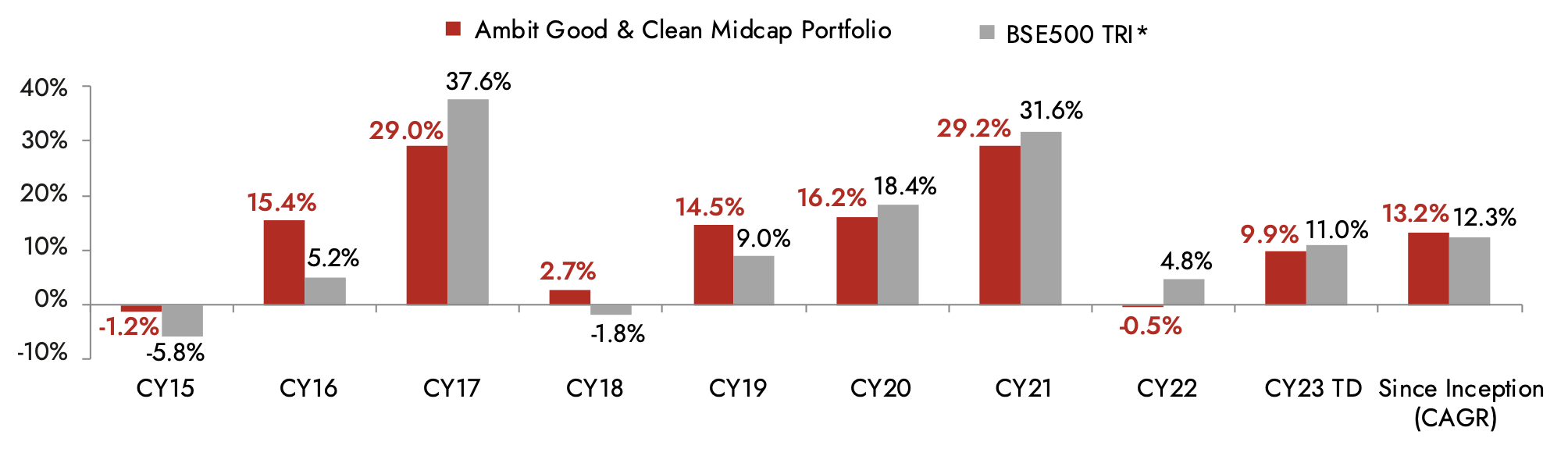

Exhibit 10: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of May 31st 2023. Returns are net of all fees and expenses.

*BSE 500 TRI is the selected benchmark for the Ambit Good & Clean Midcap strategy and the same is reported to SEBI. In addition to the same, we have included the Nifty Midcap 100 and MF Peers for information purposes only. The same should not be relied upon for performance benchmarking in any manner. MF Peers: HDFC MF, Kotak MF, SBI MF, Franklin India MF, Aditya Birla Sunlife MF, Axis MF, L&T MF, MOSL MF, ICICI Prudential MF.

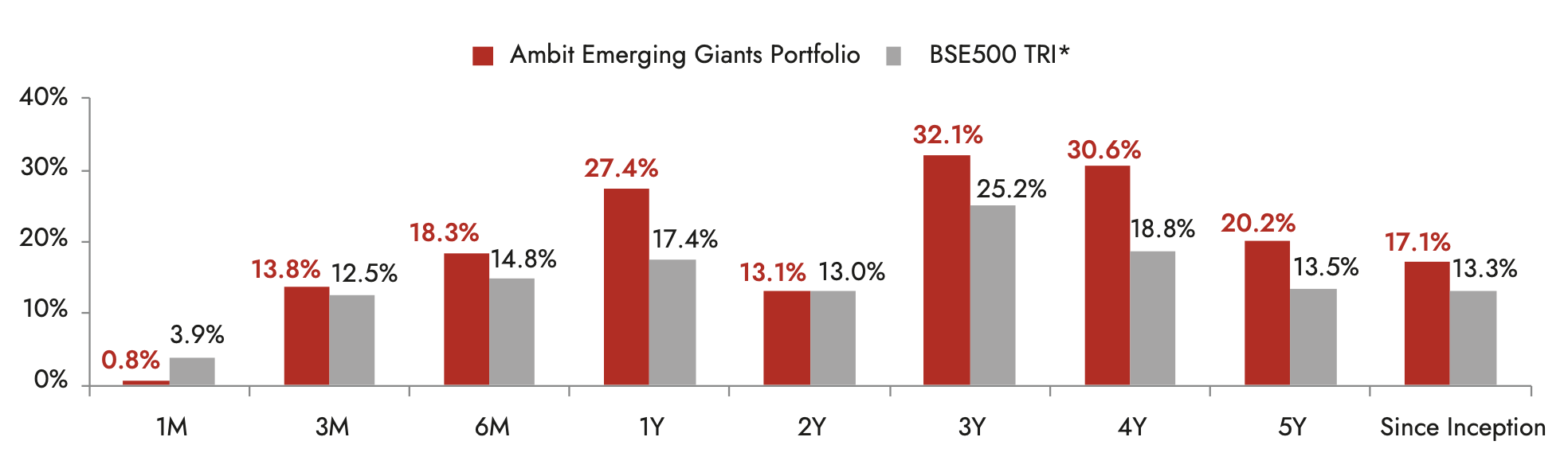

Small caps with secular growth, superior return ratios and no leverage – Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt), and the ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 11: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of May 31st 2023; All returns above 1 year are annualized. Returns are net of all fees and expenses.

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI. In addition to the same, we have included the BSE Small cap and MF Peer group for information purpose only. The same should not be relied upon for performance benchmarking in any manner.

MF Peers Include: Nippon India MF, Franklin India MF, ICICI Prudential MF, DSP Blackrock MF, Kotak MF, HDFC MF, SBI MF, Aditya Birla Sun Life MF

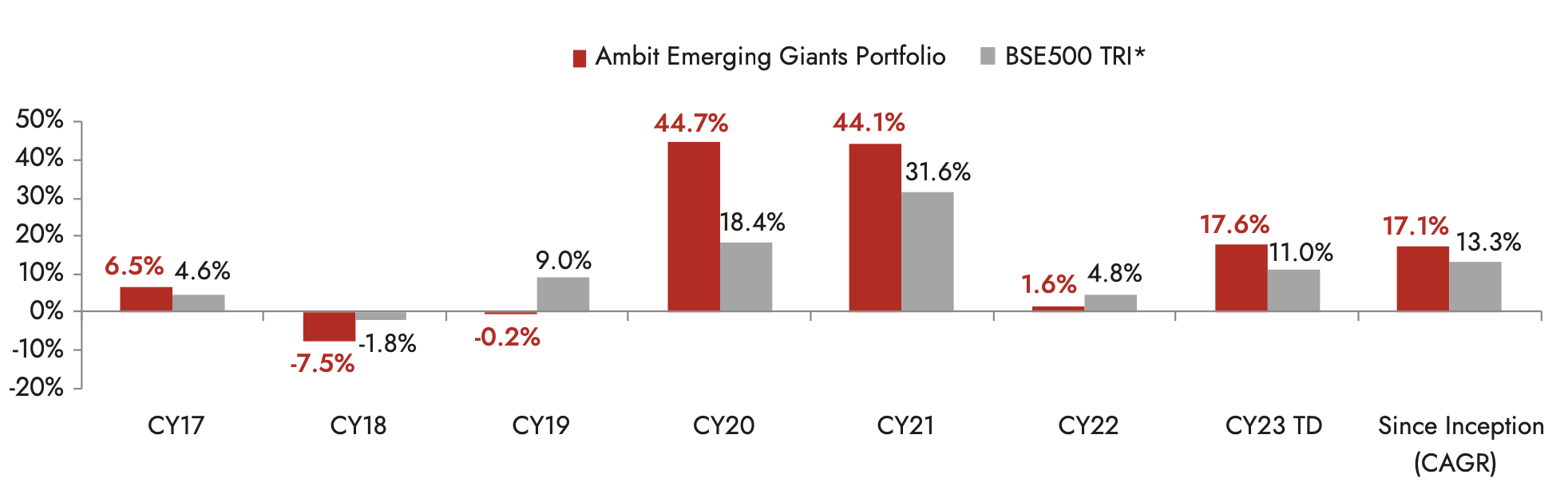

Exhibit 12: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of May 31st 2023. Returns are net of all fees and expenses.

*BSE 500 TRI is the selected benchmark for the Ambit Emerging Giants strategy and the same is reported to SEBI. In addition to the same, we have included the BSE Small cap Index and MF Peers for information purpose only. The same should not be relied upon for performance benchmarking in any manner.

MF Peers include: Nippon India MF, Franklin India MF, ICICI Prudential MF, DSP Blackrock MF, Kotak MF, HDFC MF, SBI MF, Aditya Birla Sun Life MF.

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

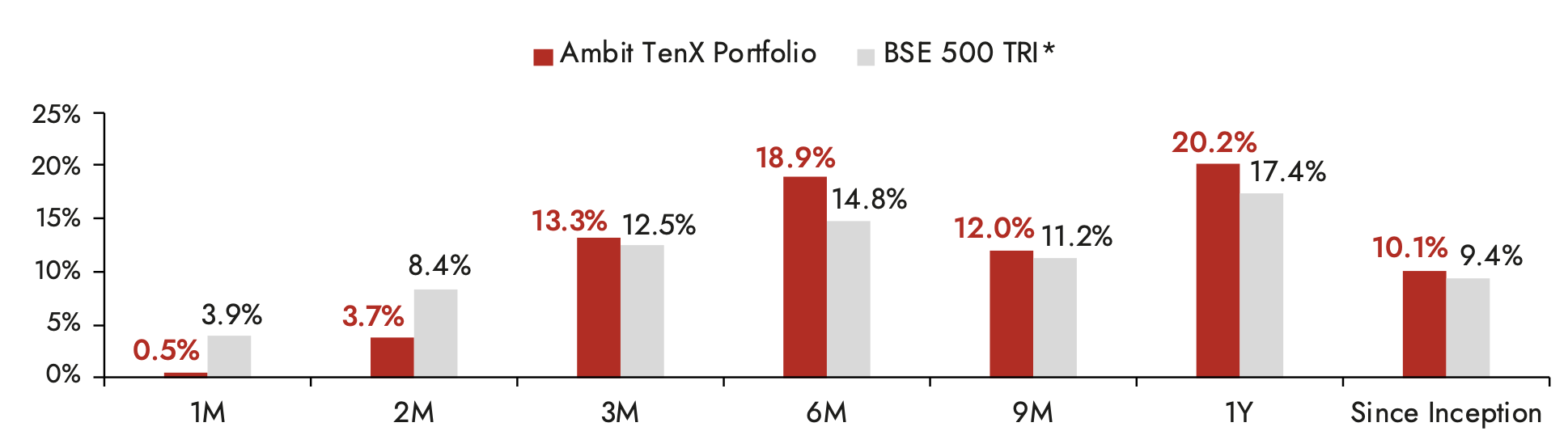

Exhibit 13: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of May 31st 2023; Returns are net of all fees and expenses

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

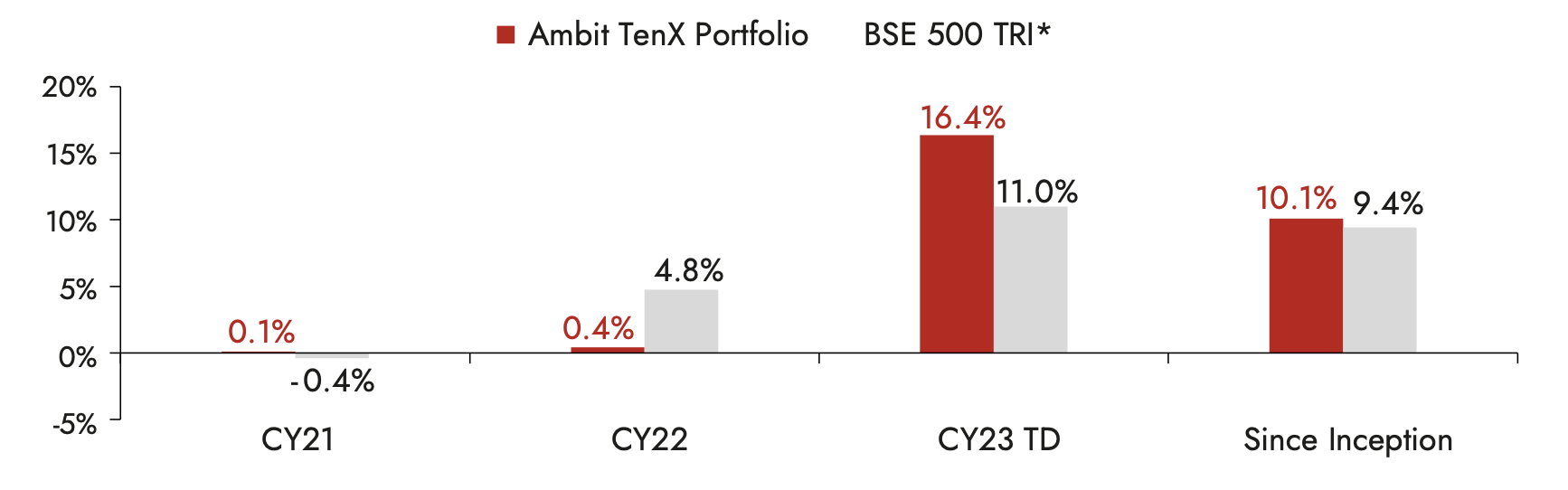

Exhibit 14: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of May 31st 2023. Returns are net of all fees and expenses

*BSE 500 TRI is the selected benchmark for the Ambit TenX Portfolio and the same is reported to SEBI.

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected]. Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020